The Case for Selling Distressed Special-Purpose Property Loans

From gas stations and quick-serve restaurants to nursing homes, hotels and athletic clubs, special-purpose properties can be great commercial real estate (CRE) loan prospects. That is, unless the business falls apart. Once that happens, foreclosure on the real estate that’s an inherent part of the business is often a costly and risky move for the CRE mortgage lender. A better solution is to sell the note—and sell it early.

In a typical scenario, the business operator begins to struggle and to violate its CRE loan terms. The business may still be a “going concern,” in accounting terms, but not thriving. To keep the business afloat, the operator may shortchange loan payments, property taxes and/or maintenance investments. The real property deteriorates as the business declines, and the property becomes a problem child for the CRE lender.

Why not foreclosure?

What defines a special-purpose property is that the business is inherently part of the collateral securing the CRE loan. If the business stops being a going concern, the property has very little remaining value. Adding complexity, going-concern properties are typically highly leveraged, almost always with first and second liens, and sometimes even a third, between SBA loans and bank loans.

If you’re the CRE lender, the combination of issues equals a colossal headache and mounting costs. A receivership can lighten the load of managing the property, processing payments, handling repairs, selecting and overseeing contractors and more.

Unfortunately, the receiver can’t remove the legal and financial risks that you assume in the foreclosure-to-REO process. Even with a third-party manager, you’re still engaged with a business that was already failing for one reason or another. That puts your institution at risk of liability for liens, negligence, environmental contamination, and more. On top of that, you face continuing labor costs to keep the business operating.

If you’re not convinced that a sale is the best option for a distressed loan on a special-purpose property, the following are examples of the risks you can encounter in a going-concern property.

Hotels in distress

Let’s start with distressed hotel mortgages. The biggest issue with the non-performing hotels mortgages that we see are usually national or global brand franchises, and the mortgage lender has no control over that flag or the brand’s requirements for franchisees.

Typically, hotel brands want owners to invest in property improvement plans (PIPs) to keep facilities in compliance with brand standards for building systems, guest rooms, amenities and more. PIPs often involve costly renovations and upgrades, but owners often lack the capital reserves to fund them—even if the business is stable, and especially if It is failing.

An owner may be able to secure a bridge loan to fund their PIP. If the owner simply can’t keep the property up to brand standards, the brand may impose hefty fines or terminate the franchisee entirely. Neither the hotel owner nor mortgage lender will have an opportunity to negotiate with the brand to determine which improvements are truly necessary to support brand quality.

So, the struggling hotel owner may lose their brand flag. Often, a hotel will struggle even more to be profitable after the brand flag is lost, and ownership may lack the cash flow to maintain the property. As the property deteriorates, it may attract crime and create negative perceptions that can last for years.

Meanwhile, if you’re the CRE mortgage lender considering foreclosure, at least half of the value of a going-concern property is in that brand flag. Rebranding and restoring operational efficiency can take a very long time and require capital.

Furthering contributing to the financial challenges is the fact that hotel operators generally not only have mortgages, but also loans for fixtures, furnishing and equipment (FFE). In foreclosure, the FFE loans become liens for which you will be responsible in foreclosure, adding to the cost.

In recent years, most brands naturally recognized that a global pandemic is not a good time for strict enforcement of PIPs. As the hospitality sector recovers, however, many are revisiting PIPs and brand standards among their franchisees, and we may see a new wave of non-performing going-concern hotel mortgages coming into the marketplace.

Underperforming gas stations

Gas stations are also problematic if the mortgage becomes distressed. First and foremost, almost every gas station has environmental contamination, even when in the hands of a good receiver, and the contamination will become your responsibility

In addition, gas station properties are typically management-intensive. Selling gasoline in itself is a low-margin business, which is why gas stations typically sell convenience items that are far more profitable. Yet, the convenience-store business that can keep a gas station afloat becomes a management headache during receivership and foreclosure.

Skilled nursing facilities

If you really want to assume risk, try foreclosing on a skilled nursing home mortgage. Nursing homes are, of course, responsible for the care of their patients-residents, and you will be, too, if you foreclose. The legal and reputational risks are enormous. You need skilled management to properly care for residents, and you also must meet state licensing requirements.

If the facility loses its state license, it will fall even more into decline—who wants their loved one to live in an unlicensed nursing facility?—and face regulatory fines. And, if standards are compromised, the general public will become aware that the facility has been cited for negligence. Once a nursing facility is perceived as treating patients poorly, it is very difficult to restore confidence—and profitability.

Why selling early is best for distressed going-concern loans

You might think that it would be difficult to sell a CRE loan backed by a struggling hotel, gas station or nursing facility. The reality is that it is far more difficult—even with a receivership—to turn these properties around or to take them through foreclosure, because your average CRE lender does not have the dedicated team and capital needed to revive a failing special-purpose property.

Once the spiral of doom begins, few lenders are equipped to handle the many legal and operational risks associated with these kinds of properties. Yet, the costs of retaining a specialized property manager, business manager, attorneys and so forth to execute a foreclosure are very high.

In our experience, you’ll wind up with as little as 20% of the original loan amount by going through the foreclosure process for a going-concern asset. By selling the loan earlier rather than later, you avoid the risks and costs.

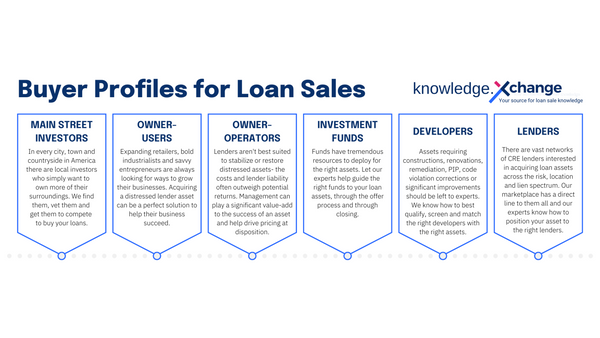

Also, you may recover more of the loan value than you expected. You might be surprised at how many potential buyers are in the marketplace looking for distressed mortgages of going-concern properties.

Potential buyers can include entrepreneurial note investors, hotel/nursing home operators, and investors that specialize in clean-up for contaminated properties to turn a property around for the good of the community. Why take on a headache—and a major loss—when you could put your distressed loan in the hands of a motivated buyer?

Want to know what your CRE NPL is worth? Try XL Value to generate a free loan valuation report.