A Pandemic, A Bank Merger & Acquisition and A Loan Sale

Drive along the shorelines of the Great Lakes and eventually you’ll see a landmark building in a scenic coastal town. Before it became a four-star assisted living facility, this unflagged hotel was visited by everyone from Theodore Roosevelt and Jane Addams to Al Capone. Despite its historical grandeur, the business fell into distress not long ago—until the timely sale of its distressed mortgage as a bank merger gave it a new future.

This architecturally significant building serving as lender’s collateral was a successful business for much of its history—but not all. Built as a seven-story hotel in the roaring ‘20s, the property was converted to senior housing in the late 1960s. Its downtown, coastal location provides stunning views of Lake Michigan, making it a desirable location for an upscale community of 130 independent and assisted living units. Additionally, over the years various owners had improved the property with a ballroom, common spaces, a full-service kitchen and a dining room.

A turn for the worst

Since 2017, The business had been 70% to 78% occupied, with 77% considered full occupancy by appraisal standards. It was operating just below full occupancy for most of 2019.

Then the COVID-19 pandemic began. In March 2020, the Michigan state government issued a moratorium on new tenants in assisted living facilities, which wasn’t lifted until November 2020. By October 2020, occupancy had declined to 45%. Although occupancy improved after the moratorium was lifted, it was still 20% below stabilized occupancy and the cash flow was too far gone for the borrower to stay current on the loans. By November 2020, the bank had issued a notice of default.

And the plot thickened. The loans matured in March 2021. The lender declined to extend, and the loans remained in monetary, technical and maturity default- OOF! So, the lender filed suit to enforce the recourse provision of the loans as compensation for the default.

Pursuing foreclosure was an option—but not a very attractive one. The foreclosure was likely to be contested, with a probable debtor-in-possession Chapter 11 filing that would eliminate any possibility of cash recovery of the outstanding debt.

A looming bank merger & acquisition

Meanwhile, the lender was about to be acquired. With a merger agreement in the works, cleaning up the balance sheet had become an urgent priority. Naturally, having a significant non-performing commercial real estate loan on the balance sheet was going to undermine the total value of the acquisition. The clock was ticking.

Given the choice between foreclosure and a loan sale in the context of a looming merger, the lender chose to sell. Learning that the loan was for sale, the borrower reached out to the bank to renegotiate.

The bank said that the way to negotiate was to place a bid in the loan sale marketplace (which was Xchange.Loans, of course) and compete for the loan. Fearful of the recourse provision, the borrower opted to pay down the $750,000 in unpaid interest and agree to a deed in lieu so that the eventual loan buyer would not enforce the recourse guaranty and pursue the borrower’s personal property for the deficiency.

A loan sale success

For the lender, the outcome was all good news. Through a targeted campaign and our accelerated process, we were able to sell the loan to a regional owner-operator committed to restoring the property to financial stability. Our rapid sealed-bid process secured a buyer and closed within four days of mutual execution of the loan purchase agreement. With the combined purchase price and a paydown of all of the outstanding interest, the lender was able to recover a significant amount of the full payoff.

Once again, when a merger is in play, one of the best moves a target bank can make is to sell its non-performing commercial real estate (CRE) loans- at higher values than their acquirer is willing to allocate, of course. For community banks, CRE loans typically constitute a large percentage of the balance sheet. If any are distressed, the impact on acquisition value can be significant.

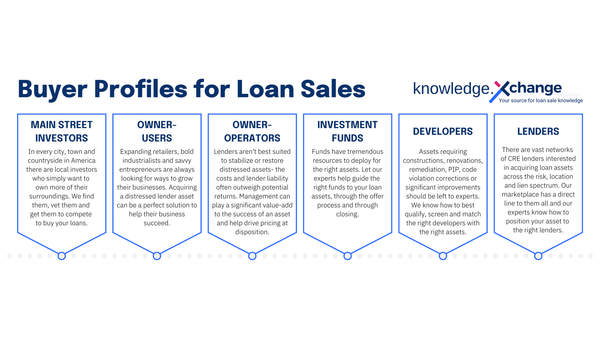

And as we’ve said before, buyer profiles matter, selling that distressed loan to the 'highest & best' buyer is the best way to recapitalize the asset, opportunity and community. When the mortgage on a prominent property in a small town becomes distressed, it’s not just a problem for the borrower—it’s a problem for the entire community. In the case of this property/loan, the local residents were proud of the property’s storied past, and appreciated the value it brought to the town as an assisted living facility. They wanted the loan and the property to land in good hands.

Today, this once-struggling senior and assisted living facility is again a profitable business serving its customers, staff and its community. And, in other good news, our bank client was so thrilled with the results of our process they regularly utilize us in their watchlist-to-disposition processes.