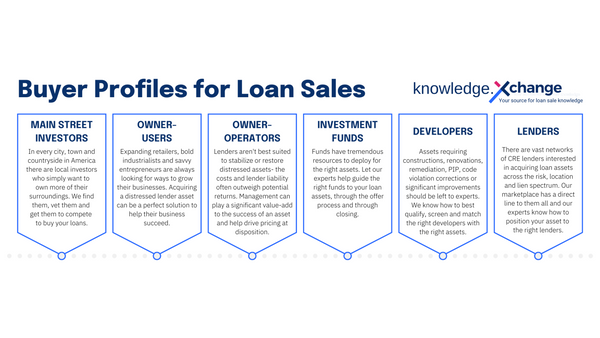

How the FDIC wins at loan sales

Whether executed online or face to face, the traditional incremental-bid auction process wasn’t designed for selling distressed commercial real estate (CRE) loans. Just ask the Federal Deposit Insurance Corporation (FDIC). The FDIC has sold billions in performing and non-performing loans without the incremental-bid auction process. Instead, the FDIC almost exclusively uses a sealed-bid process to sell failed bank loans—and there are good reasons why Xchange.Loans adopted a similar process.

As the FDIC has demonstrated, superior cybersecurity, sealed bids and multi-asset bid functionality are what make for a superior online bidding process for non-performing loans. A closer look at the FDIC loan sales process demonstrates why these practices matter. The following are key aspects that all loan sellers and buyers should understand.

Sealed-bid format for loan sales

In its function as a failed bank receiver, the FDIC sells entire portfolios of loans—performing, non-performing, residential and commercial mortgage loans, consumer and business loans. It also sells other real estate owned (OREO) by failed banks. Although the FDIC does use the traditional auction format for actual real estate assets, it does not use open, incremental bid auctions for loan sales.

For loan sales, the FDIC has adopted the sealed-bid format only, probably because FDIC policymakers understand the limitation of the traditional incremental-bid auction format. The FDIC may have recognized that loan sales buyers have varying motivations, and the sealed-bid format allows for much greater price discovery and recovery of capital than incremental bidding [more about that here]. As a public agency, FDIC knows that greater recovery of capital is good for taxpayers, too.

Bid optimization

In creating its sealed-bid process, the FDIC was looking to uncover bid dynamics. What individuals or companies are bidding? How much are they bidding? How large is the gap between the lowest and highest initial offers?

For loan sales, the sealed-bid process reveals buyer appetite much more accurately than the traditional incremental-bid process. By making it a two-phase process, the FDIC is better able to eliminate less-than-serious buyers. That’s also why Xchange.Loans adopted a two-part process—the indicative offer phase is open to all buyers, while only the highest bidders are invited to submit best and final offers.

Ultimately the FDIC—like buyers on our platform—can use market feedback to decide which offers to accept. Concurrently, buyers have a better shot at acquiring the loans they want.

Bids accepted as percentages and dollar amounts

Another smart move by the FDIC was to allow a loan buyer to place a bid that is a percentage of the loan’s unpaid principal balance (UBP), rather than bidding only in dollars. Few online platforms allow for this practice, even though it’s a smart strategy and one that note buyers prefer.

Loan buyers naturally look at the UPB of the loan as a basis for bidding. Savvy buyers know that, in distress, some borrowers will continue to pay the interest on a loan even when they can’t make their full mortgage payments, or they might continue to make partial payments on the principal while the late fees continue to accumulate. As a result, UPB can fluctuate significantly from day to day. No wonder more experienced note buyers prefer percentage bidding.

Multi-asset bidding

The FDIC also supports multi-asset bidding, in which a bidder can bid on any combination of assets in an online marketplace. Multi-asset bidding functionality is a plus for loan buyers and sellers alike, because it opens up options.

For example, imagine that a lender is selling five distressed loans on five warehouses in five different states. In a traditional incremental-bid online auction, the loans would most likely be offered in a pool, rather than as individual assets. A potential buyer might bid $0.35 on the dollar for the entire pool, since s/he can’t avoid buying the unwanted loans. For the lender, that bid would be better than nothing—but would also be a less-than-optimal outcome.

Maybe one bidder does not want all five loans, but would be willing to go as high as 80% UPB for the loan secured by a warehouse in Provo, Utah. Maybe the bidder lives in Provo and sees an opportunity to repurpose the warehouse for an arts and culture center, or to modernize it into a state-of-the-art logistics center. In either case, a platform that meets the needs of buyers is more likely to meet the needs of lenders to recapture cash, too.

A marketplace platform offering multi-asset bid functionality - like Xchange.Loans- creates more opportunities for best-value bidding. For the warehouse portfolio, for instance, a buyer could purchase all five loans or only one or two. And, the buyer could concurrently bid on other loans being marketed on the platform, rather than bidding on one loan at a time as in a traditional auction.

But wait – there’s more

Clearly, the FDIC created a great model for optimizing loan sales. Being the FDIC, however, its loan-disposition business is limited to selling assets of failed institutions. The rest of us are here to serve alive-and-well lenders that just happen to have a few distressed loans on the books.

We’ve already added to the FDIC’s foundational process with our LenderDirect self-service loan sale subscription that gives lenders complete control over over their asset dispositions with an FDIC based sealed-bid process.

LenderDirect is the first self-service loan sale service on the market offering all the loan sale tools you need, without costly brokerage and auction fees. Like the FDIC, we’re all about creating leading practices to maximize the recoverable value of your distressed loans. For us, that means making the process better and easier for you.

Sell your loan your way with LenderDirect. Contact us for more information and to request a FREE 30-day trial.