Six Ways to Sell Your Non-Performing Loans

In the best of times or the worst of times, non-performing loans (NPL) are an unfortunate fact of life for every lender in the commercial real estate (CRE) industry. What might surprise you, however, is how technology is enabling a faster, better and more cost-effective solution for converting those troubled loans into cash.

When you’re a bank with CRE NPLs, foreclosure and loan sales are the familiar options when a workout is off the table. What you may not know is that today’s loan sales can be executed more quickly, affordably and securely than ever before.

The following is a look at traditional approaches—and an introduction to today’s new way of solving your NPL problem.

1. The DIY loan sales challenge

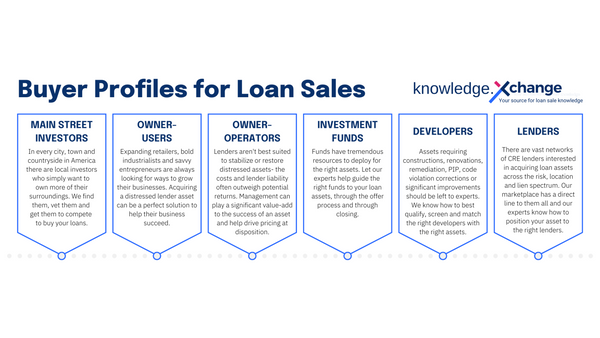

Many lenders today are looking to sell their non-performing loans to the universe of willing buyers. The do-it-yourself (DIY) loan sale is the most common disposition strategy for CRE lenders—but what you may not realize is that your go-to loan sale option has serious drawbacks.

The reality is that DIY loan sales consistently yield the worst results in terms of execution, transparency, price discovery, buyer participation, data security and efficiency. The reason is that if you’re a lender with less than $1 billion in assets under management, you probably don’t have a dedicated loan sale team, an established process, advanced loan sale software, or a network of qualified buyers committed to acquiring distressed CRE loans. And why would you? As a lender your focus is originating and servicing good loans, not getting out of bad loans.

2. Brokers aren’t loan sale experts

Working with a CRE broker or mortgage broker is another common option for lenders, but it comes with some heavy costs on top of any potential losses. Brokerage commissions, certainty of execution (or lack thereof), and a lengthy timeline are almost inevitable when you hire a broker for a loan sale. Few brokers offer dedicated loan sale advisory services, and brokerages themselves often rely on third-party auction platforms that add additional fees on top of commissions and your potential losses. As in the DIY approach, working with a broker will limit bid optimization, data security can be poor, and the lack of upfront buyer proof of funds often derails a smooth closing.

3. High-cost online auctions and wholesalers

Another limited option is to tap one of the online auction platforms that have emerged to expedite CRE transactions. However, these platforms are largely broker-driven—typically engaged as discussed above –and aren’t designed specifically for CRE loan dispositions.

Why is this important to you as a lender or servicer? For starters, your transactions costs can be as high as 10% of the loan value when you add in broker and platform fees. Also important, your data is NOT secure on most of these platforms. Furthermore, while you may receive greater bidder participation and market exposure on some these platforms than you would via DIY, the feedback these platforms provide typically isn’t in the form you need to sway your key internal decision makers to accept a sale price. Perhaps most critical, these hybrid auction-CRE brokerage sites simply weren’t designed to handle the intricate details that determine the best value for middle-market loans or mixed-asset CRE loan pools. Yet, middle-market loans—those valued at $5 million or less—comprise the majority of a typical institution’s balance sheet of performing and non-performing loans.

4. The limitations of self-service listing platforms

Of course, for the more cost-sensitive lenders, the web also offers self-service listing platforms that offer both CRE properties and loan sales. The listing platforms are typically broker-driven as well, and are designed for fee simple real estate listings with only limited marketing resources, loan sale advisory services and secure data rights management—while charging around 1% in transaction fees. They’re essentially low-cost, stripped-down, generic versions of the larger online auction and wholesale sites—without the marketing, assistance and software capabilities.

5. The painful path of foreclosure

Foreclosure is a common option for CRE NPLs—but it’s not always the right one. For starters, some commercial properties have significant environmental and going-concern liabilities that you won’t want to assume, but will inherit along with recapture of title. Aside from ownership issues, foreclosure is a time-consuming, drawn-out process, and it can be risky.

For example, state law may require your institution to request a judgment of foreclosure and order of sale via a lawsuit. The borrower may propose a deed in lieu of foreclosure, requiring your institution to undertake due diligence to uncover environmental issues, delinquent taxes, judgments, liens or other encumbrances on the property. Of course, if the outstanding indebtedness of the borrower exceeds the current fair value of the property, you may choose not to proceed with a deed in lieu—but you’re still stuck with the foreclosure process.

If the bank receives a foreclosure judgment, you may need another court order for an appointed receiver to assume responsibility for the asset until the foreclosure lawsuit is resolved. Receivership removes the risk of the borrower using the property income to, say, pay other creditors instead of the primary lien holder, or abandon any semblance of management. However, receivership also adds to the cost of foreclosure.

Either way, the path of foreclosure ultimately leaves you with ownership of the property and the need to sell to recoup any losses from the loan. The catch? Depending on the condition of the property and the market environment, the property may or may not actually sell and you may be stuck with a property you don’t want to own with less equity than you initially underwrote.

6. The power of the online open-listing marketplace

The biggest limitations of lenders’ traditional recapitalization options are engrained because none were designed specifically to help lenders exchange their loans for liquidity—especially non-performing loans. After decades of strategies both old in new, it’s becoming clear that an open and secure marketplace utilizing a call-for-offers process, similar to the FDIC’s process for bank asset dispositions—is the best strategy for lenders looking to exchange their loans for liquidity. None of the older broker- centric marketplaces properly leverage the data security, marketing and bid optimization technology now available.

The good news?

A new affordable online marketplace is now available that offers speed-to-market through the optimal loan disposition process. With its open and secure listing format, this new option empowers lenders and buyers with advanced data security, powerful marketing and proprietary bid optimization technology. Even better, lenders can now opt for lender self-service to connect with note buyers and achieve certainty of execution—and the best value for your CRE NPLs.

The reality is that neither a broker nor a licensed auctioneer is required for loan disposition. It’s time to explore a new way.

Want to know what your CRE NPL is worth? Try XL Value to generate a free loan valuation report.